Lumax Industries |2QFY2019 Result Update

October 26, 2018

LUMAX Industries

BUY

CMP

`1620

Target Price

`2500

Quarterly (` cr)

Q2FY19

Q2FY18

% yoy Q1FY19

% qoq

Investment Period

12 Months

Net sales

518

380

36%

496

4%

EBITDA

41

30

34%

41

-1%

EBITDA margin (%)

7.8%

8.0%

-13

8.2%

-26

Stock Info

Adjusted PAT

21

21

-0.2%

22

-6%

Sector

Auto-Ancillary

Market Cap (` cr)

1,515

Source: Company, Angel Research

Beta

1.3

Lumax Industries limited (Lumax), posted decent revenue growth in 2QFY2019, up 36%

52 Week High / Low

2585/1553

Avg. Weekly Volume

889

yoy to `518cr from `380cr in 2QFY2018. However, the bottom-line growth was flattish

Face Value (`)

10

owing to negative impact of foreign exchange and reduction in profit from associate.

BSE Sensex

33,690

Nifty

10,124

We believe that adoption of new technology in LED lighting and addition of newer

Reuters Code

LUMA.BO

Bloomberg Code

LUMX IN

models will aid the company to maintain the current growth rate going forward.

In 2QFY2019, share of LED remained at similar levels like that 1QFY2019; however it has

Shareholding Pattern (%)

improved from 8% in FY2017 to 35% in Q2FY19. Further, we expect margins to be in the

Promoters

75.0

range of 8.0%-8.5% at least for next 2-3 quarters, as localization of import content is yet

MF / Banks / Indian Fls

1.1

to turnaround. Moreover, we project that margins will start improving from Q2FY2020

FII / NRIs / OCBs

0.9

owing to implementation of localization coupled with increase in revenue share from

Indian Public / Others

23.0

LED lighting.

For the quarter under review, Lumax has made new launches in 2W, PV and CV. In our

Abs.(%)

3m

1yr

3yr

view, 2W segment (Destini 125-Hero MotoCorp Ltd.)) will aid revenues going forward

Sensex

(1.9)

2.0

23.1

along with other new launches like Gurkha (PV-Force Motors Ltd.) and Ape (CV- Piaggio

LUMAXIND

(28.0)

(4.1)

254.0

Vehicles Pvt. Ltd).

Outlook and Valuation: We have a positive outlook on Lumax from a long term

perspective and we expect the company to grow above the industry growth rate going

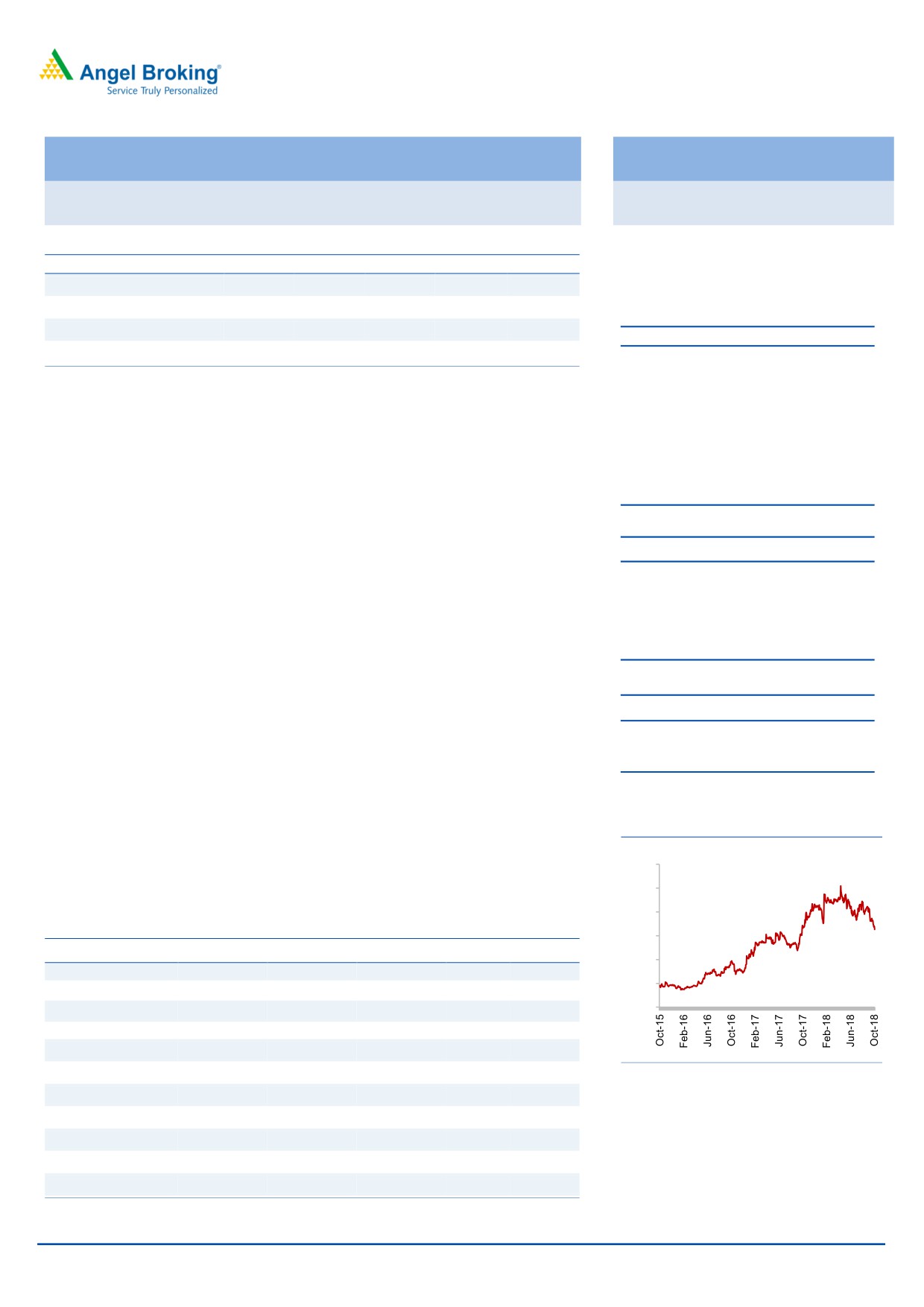

3 Years Performance charts

ahead. At the CMP of `1,620, stock is available at 14x its FY20E EPS of `119. We maintain

3000

our BUY recommendation on Lumax with a target price of `2,500 (reduced from `2,550),

2500

implying a potential upside of 54%.

2000

Exhibit 1: Key Financials

1500

Y/E March (` cr)

FY16

FY17

FY18

FY19E

FY20E

1000

Net Sales

1,255

1,271

1,650

1,980

2,336

500

% chg

10

1

30

20

18

0

Net Profit

52

54

71

84

111

% chg

2,160

4

31

18

32

EBITDA (%)

7.1%

7.9%

8.2%

8.2%

8.9%

EPS (Rs)

39

58

76

90

119

Source: Capitaline, Angel Research

P/E (x)

41

28

21

18

14

P/BV (x)

5.6

4.9

4.2

3.5

2.9

Kripashankar Maurya

RoE (%)

13.7

17.6

19.7

19.5

21.4

022 39357600, Extn: 6004

RoCE (%)

13.9

15.2

18.7

19.7

22.4

EV/EBITDA

18.1

15.7

11.9

9.7

7.6

Source: Company, Angel Research; Note: CMP as of Oct 25, 2018

October 26, 2018

1

Lumax Industries |2QFY2019 Result Update

Exhibit 1: Q2FY19 Performance

In Cr

Q2FY19

Q2FY18

Q1FY19

YOY %

QOQ%

Net Sales

518

380

496

36%

4%

Total Income

518

380

496

36%

4%

Total Expenditure

477

349

455

37%

5%

Raw Material Consumed

338

248

331

36%

2%

Stock Adjustment

4

-4

-11

NA

NA

Purchase of Finished Goods

3

2

4

82%

-24%

COGS

345

246

324

40%

6%

Employee Expenses

55

45

54

22%

3%

Other Expenses

77

58

78

32%

-1%

As a % of sales

Raw Material Consumed

65%

65%

67%

Stock Adjustment

1%

-1%

-2%

Purchase of Finished Goods

1%

0%

1%

COGS

67%

65%

65%

Gross Margin %

33%

35%

35%

Employee Expenses

11%

12%

11%

Other Expenses

15%

15%

16%

EBITDA

41

30

41

34%

-1%

Other Income

1.08

0.8

3.1

38%

-65%

Profit from Associate

1.83

6.7

3.2

-73%

-43%

Interest

3.68

1.2

3.1

220%

20%

PBDT

39.77

36.56

43.99

9%

-10%

Depreciation

13.81

11

14

20%

2%

PBT

25.96

25.09

30.45

3%

-15%

Tax

5.09

4

8

22%

-38%

PAT

21

21

22

0%

-6%

Ratios

BPS

BPS

EBITDA margin (%)

7.83%

7.95%

8.21%

-13

-38

PAT margin %

4.03%

5.51%

4.48%

-148

-45

Tax rate %

19.60%

16.65%

26.99%

295

-738

Source: Company, Angel Research

Customer wise sales mix

120.0%

100.0%

4.0%

5.0%

8.0%

9.0%

9.0%

9.0%

9.0%

8.0%

11.0%

11.0%

10.0%

10.0%

7.0%

6.0%

80.0%

7.0%

7.0%

7.0%

7.0%

32.0%

34.0%

60.0%

31.0%

32.0%

31.0%

32.0%

40.0%

22.0%

22.0%

21.0%

20.0%

21.0%

19.0%

20.0%

9.0%

11.0%

10.0%

10.0%

11.0%

11.0%

12.0%

11.0%

11.0%

12.0%

17.0%

14.0%

0.0%

Q1FY18

Q2FY18

Q3FY18

Q4FY18

Q1FY19

Q2FY19

HMSI HML

Others

Maruti

TATA

M&M HCIL

Source: Company, Angel Research

October 26, 2018

2

Lumax Industries |2QFY2019 Result Update

Q2FY2019 Key highlights of post result and concall

Lumax has reported robust revenue growth of 36% yoy to `518cr in Q2FY19

owing to strong growth from key customers viz. HMSI (76%), HML (52%) and

Maruti (47%). However, revenue from HCIL de-grew 25% yoy, as it was

unable to supply to few models like Amaze and City which have performed

well.

Despite an increase in revenue, bottom-line, on consolidated basis, remained

stable owing to forex loss of `4.3cr as against forex gain of `0.5cr in same

quarter last year, however it can be passed on to the customers post

negotiation with respective clients.

Management expects to bring down the import component of LED to 50% by

FY2020 from 65% currently, which will help to improve operating margins.

Outlook and Valuation: We have a positive outlook on Lumax from a long term

perspective and we expect the company to grow above the industry growth rate going

ahead. At the CMP of `1,620, stock is available at 14x its FY20E EPS of `119. We

maintain our BUY recommendation on Lumax with a target price of `2,500 (reduced

from `2,550), implying a potential upside of 54%.

Risks to our estimates

Downside risk to target revenue and net income is slower than expected

adoption of LED lamp by OEM’s and higher content of import raw material

respectively.

Upside risk to target revenue is faster growth in PV and 2W segments.

October 26, 2018

3

Lumax Industries |2QFY2019 Result Update

Income statement

Y/E March (` cr)

FY16

FY17

FY18

FY19E FY20E

Total operating income

1,255

1,271

1,650

1,980

2,336

% chg

10

1

30

20

18

Total Expenditure

1,167

1,170

1,515

1,817

2,128

Raw Material

767

818

1,104

1,317

1,565

Personnel

141

160

189

208

245

Selling and Administration Expenses

76

86

107

128

151

Others Expenses

183

106

115

164

166

EBITDA

89

101

135

163

208

% chg

(65)

14

34

21

28

(% of Net Sales)

7.1%

7.9%

8.2%

8.2%

8.9%

Depreciation& Amortisation

38

41

48

58

69

EBIT

51

60

87

105

139

% chg

(76)

18

46

21

33

(% of Net Sales)

4

5

5

5

6

Interest & other Charges

13

11

8

12

12

Other Income

4

17

19

21

23

Extraordinary Items

-

-

-

Recurring PBT

41

65

98

113

150

% chg

(80)

58

51

16

32

Tax

4

10

26

29

39

PAT (reported)

37

54

71

84

111

% chg

(82)

48

31

18

32

(% of Net Sales)

2.9

4.3

4.3

4.2

4.8

Basic & Fully Diluted EPS (Rs)

39

58

76

90

119

% chg

122

48

31

18

32

Source: Company, Angel Research

October 26, 2018

4

Lumax Industries |2QFY2019 Result Update

Balance Sheet

Y/E March (`cr)

FY16

FY17

FY18

FY19E FY20E

SOURCES OF FUNDS

Equity Share Capital

9.4

9.4

9.4

9.4

9.4

Reserves& Surplus

259

300

353

421

511

Shareholders Funds

268

309

362

430

520

Total Loans

95

83

101

101

101

Other Liabilities

51

32

47

50

50

Total Liabilities

415

423

510

581

672

APPLICATION OF FUNDS

Net Block

425

419

532

640

771

Capital Work-in-Progress

-

20

34

20

20

Investments

69

79

88

105

117

Long Term Loans & Advances

31

2

4

4

4

Current Assets

332

348

562

659

730

Inventories

105

116

169

212

224

Sundry Debtors

181

191

318

391

474

Cash

3

1

2

32

30

Loans & Advances

36

-

1

1

2

Investments & Others

7

40

73

24

0

Current liabilities

444

456

721

857

981

Net Current Assets

-111

-109

-159

-198

-251

Other Non Current Asset

1

11

11

11

11

Total Assets

415

423

510

581

672

Source: Company, Angel Research

Cash flow

Y/E March (`cr)

FY16

FY17

FY18

FY19E FY20E

Profit before tax

41

65

98

113

150

Depreciation

38

41

48

58

69

Change in Working Capital

(0)

7

17

(14)

(45)

Interest / Dividend (Net)

13

11

8

12

12

Direct taxes paid

4

10

26

29

39

Others

(7)

(24)

(40)

(29)

(39)

Cash Flow from Operations

89

111

157

170

186

(Inc.)/ Dec. in Fixed Assets

(38)

(63)

(132)

(119)

(149)

(Inc.)/ Dec. in Investments

1

1

4

(17)

(12)

Cash Flow from Investing

(37)

(62)

(128)

(137)

(161)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

61

-13

19

-

-

Others

(120)

(27)

(30)

(19)

(27)

Cash Flow from Financing

(59)

(39)

(11)

(19)

(27)

Inc./(Dec.) in Cash

(7)

10

17

14

(3)

Opening Cash balances

18

3

1

19

32

Closing Cash balances

3

1

19

32

30

Source: Company, Angel Research

October 26, 2018

5

Lumax Industries |2QFY2019 Result Update

Key Ratio

Y/E March

FY16

FY17

FY18

FY19E FY20E

P/E (on FDEPS)

41

28

21

18

14

P/CEPS

17

16

13

11

8

P/BV

6

5

4

4

3

EV/Sales

1

1

1

1

1

EV/EBITDA

18

16

12

10

8

EV / Total Assets

3

3

3

3

3

Per Share Data (Rs)

EPS (Basic)

39

58

76

90

119

EPS (fully diluted)

39

58

76

90

119

Cash EPS

96

102

128

152

192

DPS

0

0

14

17

22

Book Value

287

331

387

460

556

Returns (%)

ROCE

14

15

19

20

22

Angel ROIC (Pre-tax)

15

18

22

25

28

ROE

14

18

20

20

21

Turnover ratios (x)

Inventory / Sales (days)

30

33

37

39

35

Receivables (days)

53

55

70

72

74

Payables (days)

90

94

119

119

110

Working capital cycle (ex-cash) (days)

-7

-6

-11

-8

-1

Source: Company, Angel Research

October 26, 2018

6

Lumax Industries |2QFY2019 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER:

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay Stock

Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National Commodity & Derivatives

Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and Investment Adviser with SEBI. It also has

registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered entity with SEBI for Research Analyst in terms of

SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its associates has not been debarred/ suspended

by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any

compensation / managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision.

Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such

investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to

in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an

investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading

volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not

independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation or

warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavors to

update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us

from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Disclosure of Interest Statement

Company Name

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

October 26, 2018

7